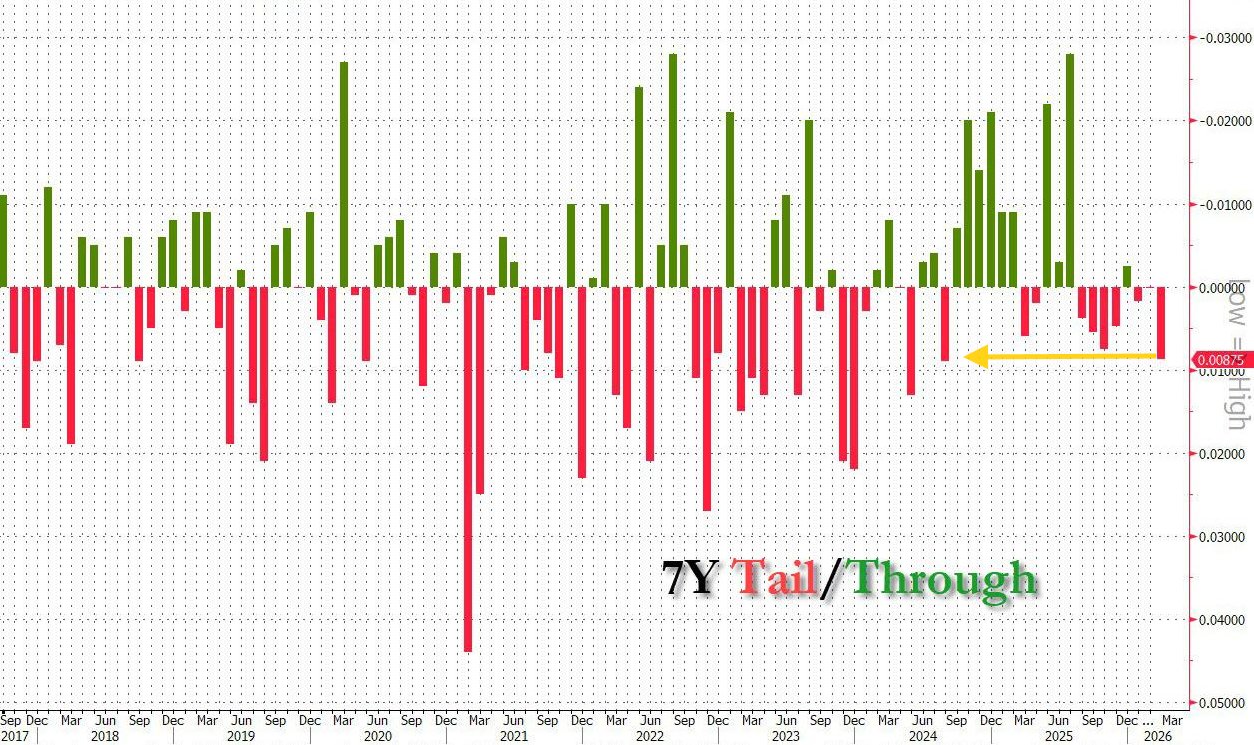

We got the 3rd (and last) of this week’s (and month’s)

#UST note auctions today w/$44bn in 7yr’s. As a reminder, we had a “terrible” and “very ugly” 2yr auction Tuesday and “another very ugly” and “terrible” 5yr auction Wednesday (both per ZeroHedge), so the bar was very low, and based on comparison it was definitely the best of the relatively bunch, even if one of the weakest in the past year.

Specifically, the bid/cover fell to 2.43, the lowest since Sept, from 2.50 in Feb and below the 6-mth avg of 2.46.

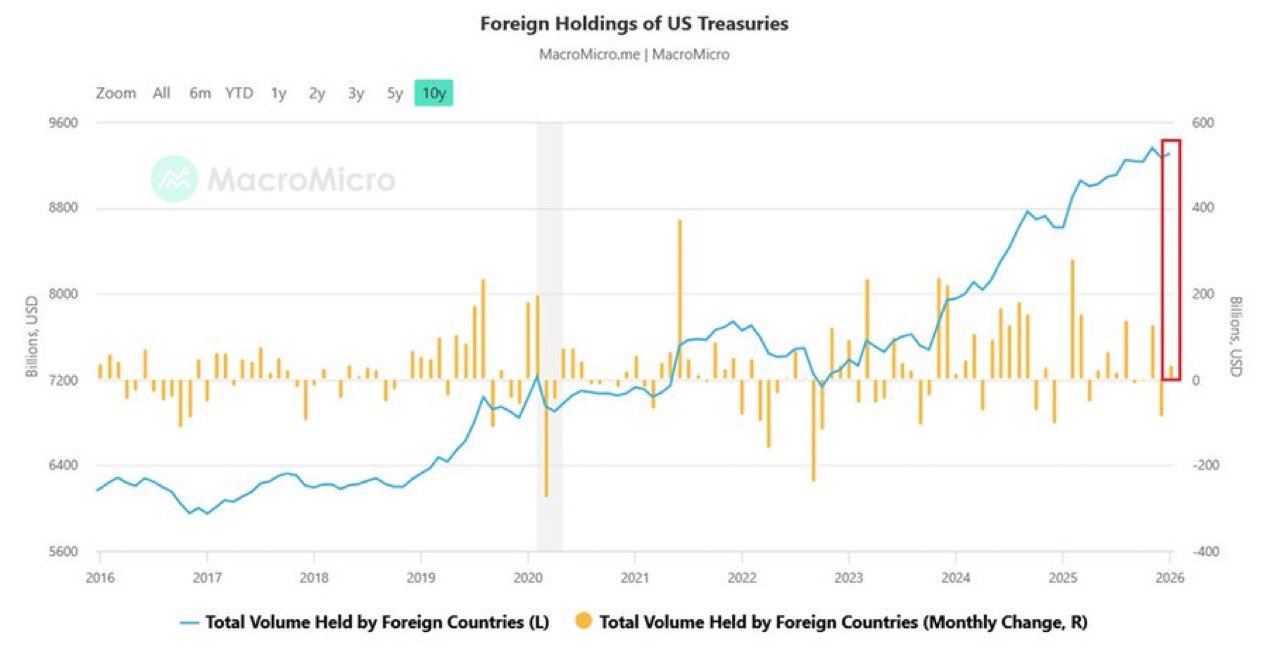

Indirect (foreign) demand fell again to 62.6%, the lowest since Dec, from 63.6% in Feb (which was down from 66.9% in Jan, the best since Aug (which was one of the highest on record at 77.5%), although up from 59.0% in Dec, 56.7% in Nov, and 56.4% in Sept (the lowest since Mar ‘21, when the auction nearly failed). It was though below the 6-mth avg of 62.6%.

Direct (domestic) demand edged down to 25.0% from 26.0% in Feb but up from 22.2% in Jan (for context the record was 33.7% in July), and below the 6-mth avg of 26.0%.

This left dealers with 12.4%, the highest since Nov, up from 10.4% in Feb and 10.9% in Jan, and above the 6-mth avg of 11.4% (for context the record low was July’s 4.1%).

The end result was a tail (yield above expectation) of +0.8bps — the biggest since August 2024 — a notable deterioration from Feb’s “on the screws” (as expected) result, now the sixth tail in the past eight auctions.

ZeroHedge called it “another very ugly auction,” noting foreign demand “wasn’t catastrophic” but was “on the light side.”

As mentioned at the top, while not great, it certainly wasn't as bad as the 2-yr or 5-yr. After a B/B- in February, this one though is a clear step back. The largest tail since Aug ‘24, lowest bid/cover since Sept, and dealers at the highest since November make this a C, but that’s a step-up from the D and D+ previously this week, and as a reminder comes in the context of the fiercest move higher in rates since SVB.