Private credit pain keeps spreading and intensifying... From the FT: "Ares has limited withdrawals from one of its marquee private credit funds pitched to wealthy individuals, as redemptions surged to 11.6% in Q1 amid a broad flight from the asset class...The decision follows f its biggest competitors, including Apollo and BlackRock...Redemptions have been accelerating this month, with funds tracked by the FT reporting $13b of withdrawal requests in Q1. The funds, which manage investment portfolios worth a combined $211b, have honoured just under 2/3rds of requests, leaving $4.6b unfilled."

As I contemplated the inevitability of a private credit reckoning in my report on "The Retailization of Private Markets", I often came back to 2022 as a reference point. To quote the report (which is available to sample here:

sageroadresearch.com/products/the-r…):

"As problematic as many private market performance claims may be, the widespread assertion that private markets are less volatile than public markets requires an even greater suspension of disbelief. It’s hard to imagine that many backers of private markets over the past decade-plus actually subscribed to the lower-volatility assertion. It’s too irrational and easy to disprove. Yes, data reported by the industry suggests private equity investments since the GFC have been far less volatile than the S&P 500. However, that’s obviously the byproduct of infrequent valuation adjustments, not a reflection of true market-value stability. In June, the FT explored 2022’s reported private credit returns as a reflection of the absurdity of private market valuations:

"The lack of trading and public data permits more…finessing around valuations and allows the industry to put up returns like the [below]. Yes, we are supposed to believe that in a year when equities and bond markets were getting brutalized—with every major segment suffering double-digit losses—private credit somehow magically eked out positive returns."

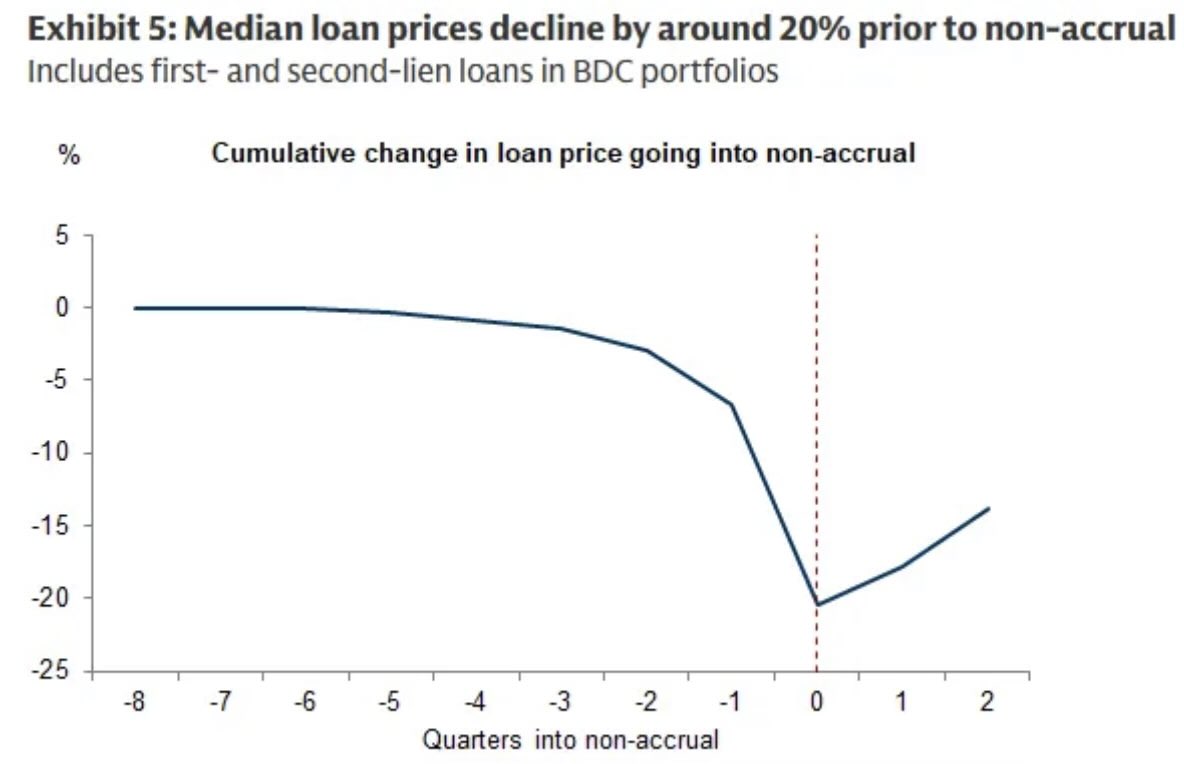

Obviously, the "SaaSpocalypse" has triggred widespread fear (an estimated 30% of all BDC portfolios are loans to software companies). From here, the question is whether fear turns to panic. To again quote the report: "By and large, most fear a similar progression: Rapid AUM growth will cause private market deal quality and debt profiles to erode. As that progresses, private market opacity will hide mounting risks, leading to a lack of awareness and in turn, a lack of accountability and market correction. That is, until significant market stress triggers accelerating fund outflows that run headlong into the inherent illiquidity of the underlying assets, causing a liquidity crisis with contagion potential. It is a progression with echoes of the GFC."

Learn more about Sage Road:

sageroadresearch.com. Interested in subscribing? Message me.

FT link:

ft.com/content/9a1b60…